Here is a hard truth that catches many families off guard when their loved one moves into a nursing home: Long-term care insurance is a specialized policy designed to cover custodial care services like room, board, and personal assistance, but it explicitly does NOT cover prescription drugs. If you bought a policy expecting it to handle your parent’s daily blood pressure meds or arthritis painkillers, you are likely looking at the wrong bill. The confusion is understandable. We tend to think of “care” as a single package. But in the U.S. healthcare system, the roof over your head and the pills in your pocket are paid for by two completely different entities.

This separation isn’t new, but it remains one of the biggest sources of financial stress for families navigating long-term care. Since the introduction of modern long-term care policies in the 1970s, and especially after the implementation of Medicare Part D in 2006, which revolutionized how prescription drugs are financed for seniors, the lines have been drawn clearly. Your long-term care (LTC) insurance pays the facility for the bed, the meals, and the help with bathing. Your health insurance-most commonly Medicare Part D-pays the pharmacy for the medication. Understanding this split is the first step to avoiding surprise bills and ensuring your loved one gets the right generic drugs without delay.

The Coverage Split: Room vs. Pills

To manage costs effectively, you need to know exactly what each policy covers. Think of it as a landlord-tenant relationship where the landlord handles the building maintenance, but you still have to pay your own utility bills separately.

Long-term care insurance typically covers:

- Custodial care (help with activities of daily living like eating, dressing, and toileting).

- Skilled nursing care if medically necessary for short periods.

- Room and board costs in a licensed nursing home or assisted living facility.

- Personal care services provided by certified aides.

It does not cover:

- Prescription medications (generic or brand-name).

- Doctor visits related to chronic conditions.

- Hospitalizations for acute illnesses (these fall under Medicare Part A or B).

According to data from the California Department of Insurance and guides from Triage Health, this distinction is rigid. Even if your LTC policy has a high daily benefit limit, say $300 a day, that money goes strictly to the facility. It does not trickle down to the pharmacy counter. This means if your loved one takes five generic medications a day, those costs are pulled from a different funding source entirely.

Who Actually Pays for Generic Drugs?

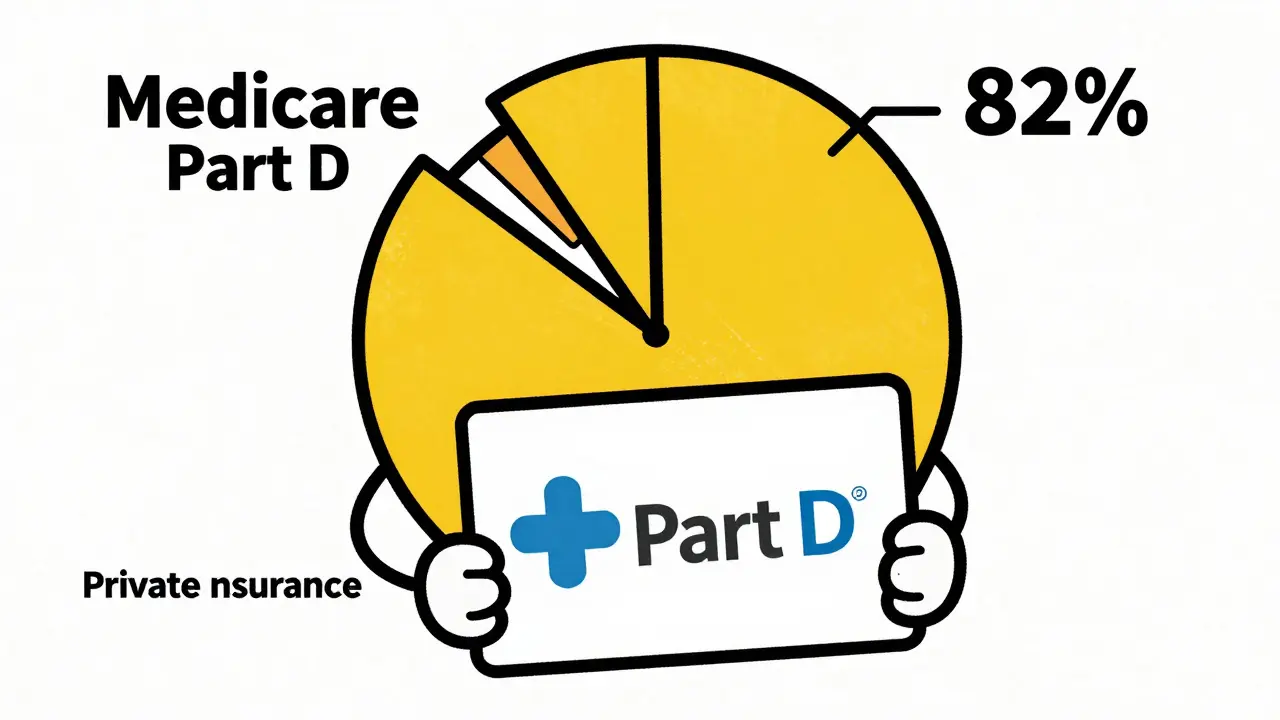

If LTC insurance doesn’t pay, who does? For the vast majority of nursing home residents, the answer is Medicare Part D is the federal program that provides outpatient prescription drug coverage to Medicare beneficiaries, serving as the primary payer for medications in long-term care settings. A 2020 study published in PMC revealed that Medicare Part D accounts for a staggering 82.4% of prescription drug coverage for Medicare enrollees in nursing facilities. Private insurance covers only 8.5%, and Veterans Administration coverage is minimal at 0.2%.

This shift happened largely because of the Medicare Prescription Drug, Improvement, and Modernization Act of 2003. Before Part D launched in 2006, about 13 million Medicare beneficiaries had no prescription drug coverage. That gap left many nursing home residents paying out-of-pocket or relying on temporary charity programs. Today, Part D is the backbone of medication financing in these facilities.

However, there is a catch. About 8.9% of long-stay Medicare enrollees in nursing homes have no detectable drug coverage. These individuals either pay entirely out-of-pocket or rely on sporadic assistance. This group represents a significant vulnerability. If your loved one falls into this category, they may face barriers to accessing even basic generic drugs due to cost constraints.

| Coverage Source | Market Share (2020 Data) | Key Characteristics |

|---|---|---|

| Medicare Part D | 82.4% | Covers both generic and brand-name drugs; requires enrollment in a private plan; subject to formularies and copays. |

| Private Insurance | 8.5% | Often secondary to Medicare; varies widely by employer or individual plan terms. |

| Medicaid | ~11.2% (for non-Medicare residents) | Pays for drugs at acquisition cost plus dispensing fee; primarily for low-income residents not eligible for Medicare. |

| Out-of-Pocket | 8.9% | No coverage; residents pay full price; highest risk for medication non-adherence due to cost. |

Navigating Insurance Formularies

Even with Part D coverage, getting the right generic drug isn’t always automatic. This is where Insurance formularies come into play. A formulary is essentially a list of approved medications that a specific Part D plan will cover. Each of the roughly 27 major Part D plan sponsors-like UnitedHealthcare, Humana, CVS Health/Aetna, Cigna, and WellCare-maintains its own formulary.

Here is the problem: Not every generic drug is on every plan’s list. While CMS mandates that plans must cover a wide range of drugs, they allow some flexibility. If your loved one needs a specific generic medication that isn’t on their plan’s formulary, the facility cannot simply order it. They must navigate an exceptions process.

In 2021, CMS implemented standardized requirements to help with this. Plans must now process non-formulary requests within 72 hours for nursing home residents. However, compliance isn’t perfect. Some plans are less likely to approve exceptions if it imposes higher costs on them. This creates a bottleneck. According to a 2019 survey by the American Health Care Association, 78% of nursing facilities spend 10-15 hours per week just managing these prescription drug coverage issues. That’s nearly $28,500 annually in staff time per facility, trying to bridge the gap between medical necessity and insurance rules.

For families, this means you can’t assume “generic” equals “always covered.” You must check if the specific generic version prescribed is on your loved one’s Part D plan formulary. If it’s not, be prepared to file an appeal or exception request immediately to avoid delays in care.

The Impact of Recent Legislation

The landscape for drug coverage is shifting again, thanks to the Inflation Reduction Act of 2022. This legislation introduces changes that directly affect nursing home residents starting in 2025 and 2026.

First, Medicare will begin paying the full cost of vaccines recommended by the Advisory Committee on Immunization Practices. This removes a small but notable out-of-pocket expense for flu shots and pneumonia vaccines. More significantly, starting in 2025, Medicare Part D beneficiaries will pay no more than $2,000 out of pocket for prescription drugs annually. This cap is a game-changer for residents with multiple chronic conditions requiring several generic medications. Previously, the “donut hole” coverage gap could lead to unpredictable and high costs. Now, there is a hard ceiling.

However, challenges remain. Dr. David Grabowski, a professor of health care policy at Harvard Medical School, notes that while Part D has improved coverage, the lack of standardization across plans still creates confusion. Furthermore, rural areas face unique hurdles. A 2022 report from the Rural Health Research Gateway found that 22% of rural nursing homes struggle to find long-term care (LTC) pharmacies that contract with all major Part D plans. In urban areas, that figure drops to 8%. If your loved one is in a rural facility, verifying pharmacy contracts is even more critical.

Practical Steps for Families

So, what should you do to ensure smooth medication management? Here is a checklist based on current best practices:

- Verify Part D Enrollment: Confirm that your loved one is actively enrolled in a Medicare Part D plan. Do not assume this happened automatically during their initial Medicare enrollment.

- Check the Formulary: Get the name of the specific Part D plan. Visit the plan’s website or call their customer service line to check if the prescribed generic drugs are on the formulary. Look for tier levels; lower tiers usually mean lower copays.

- Confirm Pharmacy Contracts: Ask the nursing home which LTC pharmacy they use. Then, verify that this pharmacy has a contract with your loved one’s Part D plan. If they don’t, the plan may refuse to pay, leaving the family liable.

- Understand the Exceptions Process: If a needed drug is not on the formulary, ask the facility’s social worker or pharmacy liaison how to file a prior authorization or formulary exception. Know the 72-hour turnaround rule.

- Monitor Out-of-Pocket Costs: Keep track of spending toward the $2,000 annual cap introduced by the Inflation Reduction Act. This helps you anticipate when you might hit catastrophic coverage, where costs drop significantly.

Facilities that excel at this often use electronic systems integrated with multiple Part D formularies and have dedicated pharmacy liaison staff. These measures can reduce medication access delays from an industry average of 3.2 days to just 0.7 days. Advocate for your loved one by asking the facility about their processes for handling formulary conflicts.

Conclusion: Managing the Dual System

Long-term care insurance and prescription drug coverage operate in parallel but separate lanes. One pays for the care environment; the other pays for the chemical interventions. By understanding that generic drug coverage falls under Medicare Part D (or private/Medicaid alternatives), not LTC insurance, you can avoid costly surprises. Stay proactive about formularies, leverage the new out-of-pocket caps, and work closely with the facility’s pharmacy team to ensure your loved one receives uninterrupted care.

Does long-term care insurance cover any medications?

No. Long-term care insurance policies are designed to cover custodial care services such as room, board, and personal assistance. They explicitly exclude coverage for prescription drugs, whether generic or brand-name. Medications are covered by separate health insurance plans, primarily Medicare Part D.

What happens if my loved one's generic drug is not on their Part D formulary?

If a drug is not on the formulary, the nursing home must initiate a formulary exception process. Under CMS rules, plans must process these requests within 72 hours for nursing home residents. If approved, the plan will cover the drug. If denied, you may need to appeal or consider alternative medications covered by the plan.

How much do I pay out-of-pocket for drugs in a nursing home?

Starting in 2025, the Inflation Reduction Act caps annual out-of-pocket costs for Medicare Part D beneficiaries at $2,000. Before hitting this cap, you will pay copays or coinsurance depending on the drug's tier in your plan's formulary. Generic drugs typically have lower copays than brand-name medications.

Which insurance covers drugs for Medicaid patients in nursing homes?

For residents who are dually eligible for Medicare and Medicaid, Medicare Part D generally covers prescriptions. For those covered only by Medicaid, the state Medicaid program pays for prescription drugs, typically at acquisition cost plus a dispensing fee. Always verify eligibility status as it determines the payer.

Why is it important to check if the LTC pharmacy contracts with my Part D plan?

Part D plans only reimburse pharmacies that have a valid contract with them. If the nursing home's LTC pharmacy does not contract with your specific Part D plan, the plan may refuse to pay for the medications. This could result in the family being billed directly or delays in receiving essential drugs until a contracting pharmacy is identified.