Have you ever stared at a pharmacy receipt and felt your stomach drop? You are not alone. For decades, Medicare beneficiaries faced a terrifying financial cliff known as the "donut hole." But if you are navigating Medicare Part D in 2026, that specific nightmare is officially history.

The landscape of senior medication coverage has shifted dramatically. Thanks to the Inflation Reduction Act, the rules changed on January 1, 2025, and they are settling into a new normal for 2026. The most critical change? A hard cap on what you pay out of pocket. No more guessing games. No more unlimited bills for life-saving drugs. This guide cuts through the bureaucratic noise to explain exactly how your drug coverage works now, where you can get extra help, and how to stop overpaying for prescriptions.

How the New Part D Structure Works in 2026

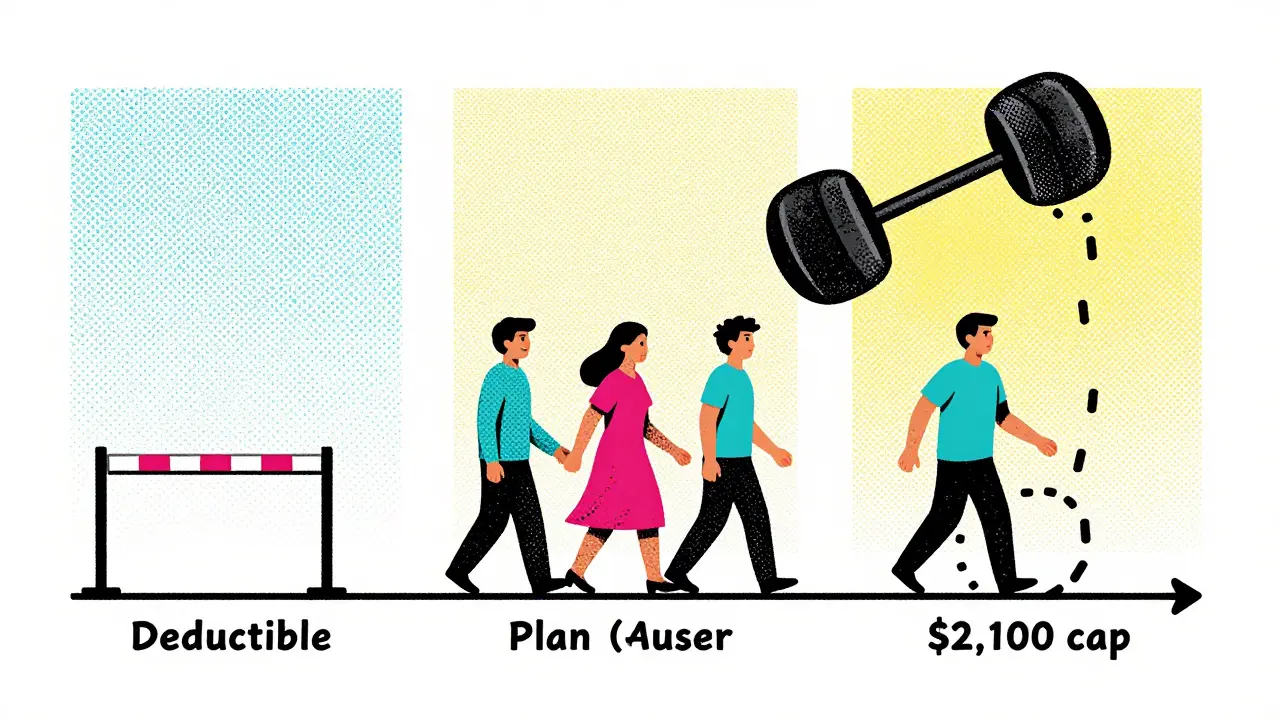

To understand your costs, you need to know the phases. The old system had four confusing stages. The new system is simpler, with three clear phases. Here is how the money flows when you fill a prescription in 2026.

Phase 1: The Deductible

You pay 100% of your drug costs until you hit the annual deductible. For 2026, this amount is indexed slightly higher than last year. While the standard maximum deductible is around $590 (adjusted for inflation from 2025), many plans offer lower or even $0 deductibles. If you choose a plan with a $0 deductible, you skip this phase entirely and move straight to Phase 2.

Phase 2: Initial Coverage

Once you pass the deductible, you enter the initial coverage period. Here, you typically pay 25% of the drug’s cost as coinsurance or copayment. The Part D plan pays 65%, and the drug manufacturer contributes 10%. This shared responsibility keeps your monthly bill predictable while you accumulate spending toward the cap.

Phase 3: Catastrophic Coverage (The Cap)

This is the game-changer. In previous years, hitting the "coverage gap" meant paying a larger share of costs until you qualified for catastrophic coverage. That gap is gone. In 2026, once your total out-of-pocket spending (deductible + copays + coinsurance) reaches $2,100, you hit the cap. After that point, you pay $0 for covered medications for the rest of the year. The plan, manufacturers, and Medicare split the remaining costs. This cap provides financial security that simply did not exist before 2025.

| Phase | What You Pay | Key Thresholds (2026 Estimates) |

|---|---|---|

| Deductible | 100% of drug costs | Up to ~$590 (varies by plan) |

| Initial Coverage | 25% coinsurance/copay | Until you reach $2,100 OOP |

| Catastrophic | $0 | After $2,100 OOP limit |

Stand-Alone PDP vs. Medicare Advantage: Which Is Right for You?

You have two main ways to get drug coverage. Understanding the difference is crucial because it affects not just your pills, but your entire healthcare experience.

Stand-Alone Prescription Drug Plans (PDPs)

These plans add drug coverage to Original Medicare (Part A and Part B). They are sold by private insurers like UnitedHealthcare, Humana, and CVS Health-Aetna. In recent years, the number of stand-alone PDPs has shrunk significantly due to market consolidation. You might find fewer options in your area compared to five years ago. However, PDPs give you the freedom to see any doctor who accepts Medicare without network restrictions.

Medicare Advantage Drug Plans (MA-PDs)

These are all-in-one plans that bundle Part A, Part B, and Part D. Many also include vision, dental, and hearing benefits. MA-PDs have grown explosively, now covering more than half of all Part D enrollees. The trade-off? You usually must use providers within a specific network. If your preferred specialist is out-of-network, you could face high costs or denied care. Always check the provider list before enrolling.

Extra Help and Low-Income Subsidies

If your income and resources are limited, you might qualify for Extra Help (also called the Low-Income Subsidy or LIS). This federal program is a lifeline for approximately 14.5 million beneficiaries. It is not just a small discount; it fundamentally changes your cost structure.

If you qualify for full Extra Help:

- You pay little or nothing for your monthly Part D premium.

- You pay no deductible.

- Your copayments are capped at very low amounts (often $3-4 per generic drug and slightly more for brand-name drugs).

- You never fall into a coverage gap because the subsidy covers those costs.

Qualification depends on your income and assets. For 2026, single individuals generally qualify if their income is below roughly $22,000 annually and their countable resources are under $16,000. Married couples filing jointly have higher thresholds. You do not always need to apply manually; if you receive certain Social Security benefits, you may be automatically enrolled. Check your status via the Social Security Administration website or call them directly.

Special Savings: Insulin and Shrink Wrap Discounts

Beyond the general cap, specific protections exist for high-cost necessities. If you manage diabetes, listen closely. The Inflation Reduction Act capped the cost of insulin at $35 per month for a 30-day supply. This applies whether your insulin is covered under Part D or Part B (if administered in a clinic). This single change saves diabetic seniors an average of over $1,000 annually.

Additionally, look for "shrink wrap discounts" or manufacturer coupons. Some drug companies still offer direct-to-consumer savings cards that can lower your copay further, though these must be used carefully to ensure they count toward your $2,100 out-of-pocket cap. Generally, payments made by third-party charities or non-governmental organizations do not count toward the cap, so stick to plan-approved discounts when possible.

How to Find the Cheapest Plan for Your Meds

Choosing a Part D plan is not one-size-fits-all. A plan with a $10 premium might charge you $50 for your blood pressure medication, while a $30 premium plan charges $5. To save money, you must compare based on your specific drug list.

- Gather Your List: Write down every medication you take, including dosage and frequency. Include generics and brand names.

- Use the Plan Finder: Go to Medicare.gov and use the Plan Finder tool. Enter your zip code and medication list. The tool will show you estimated annual costs for each plan, including premiums plus drug costs.

- Check the Formulary: Ensure all your drugs are covered. Look for tier levels. Tier 1 (generics) is cheapest; Tier 4/5 (specialty drugs) is most expensive. If a drug is not on the formulary, ask your doctor about therapeutic alternatives that are.

- Verify Pharmacy Networks: Does the plan cover your local pharmacy? Using an out-of-network pharmacy can void discounts or increase costs significantly.

Do not rely on auto-renewal. CMS data shows that 83% of beneficiaries renew without reviewing alternatives. This habit often leads to paying more. Take 3-5 hours during Open Enrollment (October 15 - December 7) to review your options. If you miss this window, you can only change plans during a Special Enrollment Period triggered by life events like moving or losing other coverage.

Common Pitfalls to Avoid

Even with better rules, mistakes happen. Here is what to watch out for.

The Premium Trap

Premiums do not count toward your $2,100 out-of-pocket cap. Only deductibles, copays, and coinsurance count. So, a plan with a very low premium but high copays might actually cost you more in the long run if you have chronic conditions requiring daily meds.

Ignoring Prior Authorization

Some plans require your doctor to get permission before the plan covers a drug. If your doctor doesn’t submit this paperwork, your claim gets denied, and you pay the full price. Keep track of which drugs require prior authorization.

Assuming All Insulins Are Capped

While most insulins are capped at $35, some older or less common types might have different rules depending on the plan. Verify the specific insulin product name on your formulary.

Is there a true limit on what I pay for Medicare Part D drugs in 2026?

Yes. There is a hard out-of-pocket cap of $2,100 for 2026. Once you spend this amount on deductibles, copayments, and coinsurance, you pay $0 for covered drugs for the rest of the year. Note that your monthly premiums do not count toward this cap.

Can I switch my Part D plan anytime?

Generally, no. You can only change plans during the Annual Election Period (October 15 - December 7) or during a Special Enrollment Period. Special periods are triggered by qualifying life events such as moving to a new service area, losing employer coverage, or qualifying for Extra Help.

How does Extra Help affect my out-of-pocket cap?

If you have Extra Help, you rarely reach the $2,100 cap because your copayments are already extremely low (often under $4 per prescription). The cap primarily protects those who do not qualify for Extra Help but have high drug costs.

Does the $35 insulin cap apply to all diabetics?

It applies to almost all commercially available insulins covered by Medicare Part D or Part B. However, you must confirm that your specific insulin brand and formulation are included in your plan’s formulary to ensure the cap applies.

What happens if my drug is not on the plan's formulary?

You may have to pay the full cost out of pocket, which does not count toward your $2,100 cap. Alternatively, you can work with your doctor to request an exception or switch to a similar drug that is covered. During Open Enrollment, you can switch to a different plan that covers your medication.

look i live in australia and our system is basically free for seniors so this whole drama about caps and deductibles seems like a first world problem to me. you americans just love complaining about the government while ignoring that at least you have SOME coverage unlike people here who get ripped off by private insurers without any federal safety net. its pathetic really.

The notion of a "cap" is merely a semantic illusion designed to placate the anxious masses; one must consider the ontological weight of bureaucratic obfuscation. The $2,100 figure is arbitrary, a construct of neoliberal policy rather than an inherent truth of healthcare economics. Furthermore, the distinction between Phase 2 and Phase 3 is philosophically dubious, as both represent a surrender of individual autonomy to the collective machinery of state-sponsored insurance. One wonders if the true cost is financial or existential.

I really appreciate this breakdown because it actually makes sense! As someone helping my dad navigate his meds, the part about checking the formulary tiers was a huge eye-opener. We were paying way too much for a brand name when a generic was right there on Tier 1. It’s wild how many people just auto-renew without looking. Thanks for sharing this, it’s going to save us a ton of stress during Open Enrollment next year. 🌟

this is all fake news anyway. they will just raise the premiums so high that nobody can afford them and then the cap doesn't matter because you cant even enroll. typical government lie. i refuse to believe anything they say about saving money. its always a trap. why should i trust this guide? its probably written by some lobbyist trying to sell more plans. dont fall for it.

You know what really gets my goat? The fact that people are still surprised by this stuff after decades of warnings. It’s not rocket science, folks. If you’re not reading the fine print, you’re getting played. I’ve seen neighbors lose thousands because they assumed their plan covered everything. It’s lazy. It’s irresponsible. And honestly, it’s morally bankrupt to expect the system to hold your hand forever. Do your homework or don’t complain when the bill comes. Simple as that.

omg thank you for posting this!!! i was so confused about the insulin cap and now i feel so much better :) my mom has diabetes and we were worried sick about the costs. knowing its capped at $35 is such a relief. i hope everyone reads this carefully so they dont miss out on savings. stay safe out there! ❤️

i mean like duh right?? why would anyone pay more than they have to? its basic human nature to want cheap meds. but seriously the whole prior authorization thing is a nightmare. my doc had to fight for weeks just to get approval for my blood pressure med. its ridiculous that we have to jump through hoops just to stay alive. the system is broken and needs fixing ASAP.

It is imperative to understand that the nuances of Medicare Advantage versus Stand-Alone PDPs are not merely administrative details but fundamental choices that dictate the trajectory of one's healthcare experience. Many individuals fail to grasp the significance of network restrictions, leading to catastrophic financial outcomes when they require specialized care outside their designated provider list. Furthermore, the assumption that a lower premium equates to lower overall cost is a fallacy that plagues the majority of enrollees, resulting in significant regret during the annual review period. One must meticulously analyze the formulary tiers and pharmacy networks to ensure alignment with their specific medical needs.

Please note that Extra Help applicants should verify their eligibility status annually; income thresholds adjust slightly each year. It is crucial to distinguish between full LIS and partial LIS benefits, as the copayment structures differ significantly. For those managing chronic conditions, the $2,100 cap is a vital safeguard, yet it does not replace the need for strategic plan selection. Always consult the Plan Finder tool on Medicare.gov to compare projected annual costs based on your actual medication usage patterns.

this is such a game changer for seniors!! 🙌 the fact that the donut hole is gone is amazing. i tell all my friends to check their formularies every october because things change so fast. dont let them charge you more than you need to pay. knowledge is power! 💪✨

It is absolutely unacceptable that beneficiaries are still required to navigate this complex maze of phases and caps. The burden should not rest on elderly individuals to decipher actuarial tables. While the cap is a step forward, the lack of transparency in premium pricing remains a critical flaw. We demand clearer communication from CMS regarding these changes. Until then, citizens must remain vigilant against predatory marketing tactics. 😠

i just checked my plan and realized i was in the wrong tier for my heart meds. switching to a different plan saved me over $200 a year. glad i read this before renewal time. thanks for the tip on using the plan finder tool it was super easy to use.

As a healthcare data analyst, I can confirm that the utilization metrics for Part D have shifted dramatically post-IRA implementation. The reduction in out-of-pocket exposure correlates with increased adherence rates for chronic therapies. However, the administrative overhead for providers processing prior authorizations has increased by approximately 15%. This operational inefficiency is a significant pain point in the current ecosystem. 📊📈